“Customer experience is chief among the areas where traditional financial institutions have fallen short. 70% of millennials would rather visit their dentists than their bankers.” Harit Talwar, Head of Marcus at Goldman Sachs.

Not long ago, wealth management was considered a service almost exclusively confined to the affluent. With their millions at the ready, wealthy investors could use wealth managers to provide a range of tailored investment-related services, and those services would normally come at a high price.

But these days, such a perception of wealth management is becoming old, or simply not accurate. Innovation broke down those barriers of exclusivity, enabling services that were previously only accessible to the privileged few to be in the hands of the masses of ordinary investors.

And not just ordinary investors. Young investors, too. With wealthtech, tech-savvy youngsters are driving a seismic shift in the way wealth is being managed…

Wealthtech falls under fintech as a segment which specifically focuses on technology that aims to transform wealth management and retail investment. It involves the application of digital solutions to wealth management, ultimately providing new channels to deliver more efficient, cost-effective and efficient services to customers.

Cost savings result from greater automation of processes, streamlining of asset allocation, and more centralization of portfolio management.

Children – The Future…

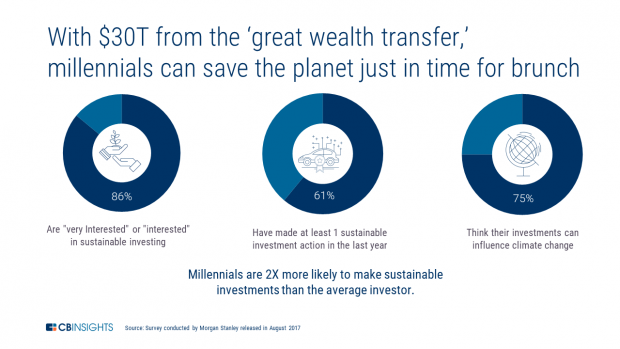

It also seems that the younger Millennial generation will drive much of the progress in wealthtech. According to a recent analysis from CBInsights, “Millennials stand to inherit approximately $30T from their parents, the baby boomers, in the coming decades….” The research specialist also projects that by 2030, this group will hold 5 times as much wealth as they do today.

So, an enormous amount of capital is potentially up for grabs, and “both upstarts and advisors are vying for a piece of the pie.” But given their distaste for traditional, legacy institutions, it may well be the ‘upstarts’ that win this particular battle.

Should firms continue serving the Millennials using the same, antiquated strategies that might have worked well on Baby Boomers, it seems highly unlikely that they will succeed.

Indeed, technology is already helping Millennials make smarter investing decisions, especially via the biggest and most visible categories of wealthtech.

-

Robo-Advisory

To date, it’s robo-advisory that has had the greatest impact within the wealthtech sphere. This hugely popular form of digital wealth management involves a greater degree of automation than traditional asset management, whereby machine learning algorithms – rather than human advisors – are employed to determine the optimal portfolio allocation for each investor.

The mere fact that much of the process is online means the staffing costs can often be reduced. That said, most research suggests that the majority of robo-advisory customers prefer a combination of automation and human advice, i.e. a hybrid model, of which The Vaguard Group, Betterment, and Personal Capital are some of the leading providers.

We have previously discussed how robo-advisors are changing the industry. But other types of wealthtech are now emerging to expand the definition of this particular segment, and importantly, they are disrupting almost every important stage of the value chain.

-

Robo-retirement

A subset of robo-advisory that has boomed in popularity in the US, Robo-retirement companies are applying tech to manage retirement savings accounts including 401(k), 403(b), and IRA.

An example of a retiree robo-advisor is United Income, which deals exclusively with services tailored for retirement. In addition to the automated investment platform it provides in the same vein as a typical robo-advisor, the company also provides specific retiree-related services, such as the “retirement paycheck” which helps customers budget their money in a similar manner to when they were receiving a regular income, a one-time financial plan, and assistance with Social Security and Medicare.

Much like hybrid robo-advisors, therefore, most robo-retirement services involve both automated and human components.

-

Micro-investment

As investment becomes more accessible, it must also become more flexible to the greater variety of investor profiles. As such, the minimum investment threshold is being slashed across numerous markets, and through a variety of mechanisms.

Micro-investing is one such mechanism. It means saving, depositing, and investing small sums of money into an investment account, thus removing some of the traditional barriers of investing such as trading fees and minimum balance requirements. And it can usually be done very conveniently using a smartphone.

Two companies have emerged as leaders in this field so far – Acorns and Stash Invest. Both are available as mobile apps on iOS and Android, and allow you to invest very little each time. Indeed, Acorns has no minimum deposit requirement, while Stash’s minimum is $5. But Stash does provide access to a much larger range of exchange-traded funds (ETFs).

Given the well-publicized issues millennials face with saving sufficiently for the future, micro-investing provides a very useful channel to help them save small amounts of money regularly. As such, it may well make investing more convenient and manageable for those with less to spare.

-

Digital Brokerage

Trading is now more accessible than ever. And that means anyone can obtain the tools required to invest in an informed manner. We have recently observed the rise of social trading platforms such as eToro as one of the main ways in which this accessibility is being boosted.

Other digital brokers such as Robinhood allow investors to participate in markets and invest in funds without paying the traditionally exorbitant commissions. According to the company itself, it “was built from the ground up to be as efficient as possible. By cutting out the fat — hundreds of storefront locations, manual account management, expensive Super Bowl ads, etc. — Robinhood is able to maintain a lean bottom-line and pass the savings along to the customer.”

Traditional brokers are now also moving into this space by adding a digital service to their suite of offerings. Normally, this new service will be cheaper than the traditional versions, with some services excluded to compensate for the cost saving.

-

Portfolio Management

This involves innovative tools that allow investment portfolios to be managed on a single platform, for the benefit of both investors and financial advisors. This helps both parties monitor, analyze and generally better manage portfolios.

Grisbee is a wealthtech company providing such tools. It offers an online portfolio management platform for investors to bring their various accounts together for more convenient monitoring, as well to receive tailored advice on their investments.

-

Investment Tools

These are various tools that can be accessed by investors to obtain useful investment information.

For example, Nerdwallet enables access to a network of investing experts, it provides comparisons of digital brokers on the market and products available from various banks and insurance companies. And Kensho is using a powerful AI platform to analyze masses of potentially market-moving data to find relationships between world events and their impact on market prices across various assets.

-

Financial Services Software

Companies are now providing specialized software to customers such as banks and fintech start-ups that supports adoption of digital wealth management and investment strategies.

Plaid Technologies, for example, builds APIs to connect consumers, traditional financial institutions, and developers. App users, for instance, can be connected to their bank accounts using Plaids software.

And as new, more burdensome regulatory requirements have come into effect recently, wealthtech companies are also heavily focusing on providing enhanced risk management software to wealth management firms.

A Segment to Watch

The startling success of many of these companies underlines just how popular wealthtech is proving to investors, financial services companies and fintech start-ups. And its utility is further reflected by the sharply rising investment that it’s now receiving:

Speculation hovers over whether human investment managers will become marginalized once wealthtech evolves to a sufficiently advanced level of automation. But let’s be clear, robots are not about to take wealth managers’ jobs anytime soon. The rich and super-rich (or HNWs and UNHWs) will still require the personal, nuanced inputs of financial advisors, no matter how smart automated services become.

As Forbes recently cited John Bowen, founder of CEG Advantage and author of Elite Wealth Planning: Lessons from the Super Rich, who conducted over 30 years of extensive empirical research: “the most significant success factor in the financial advisory business is the human element. It is the personal and emotional component of wealth management. It addresses everything and everyone that is important to the affluent individual or family in addition to everything and everyone that could be affected by the wealth management solutions.”

If you’re looking to get started on your investment journey, I highly recommend this beginners guide!

The stat on “70% OF MILLENNIALS WOULD RATHER VISIT THEIR DENTISTS THAN THEIR BANKERS.” is not surprising. Millennials aren’t looking for the traditional wealth management route. Men in suits are now seen as a taboo than professional to the younger generations. The future is in fintech. There needs to be an online wealth management system that almost gamified and also allows for a purposeful investment to capture to younger market.