“Venture Capital In Q1 2019: The World Pulls Back From Record Highs.”

“Apple buys self-driving startup Drive.ai just days before it would have died.”

“China’s historic car market decline continues, as trade war and emissions clampdown hit sales.”

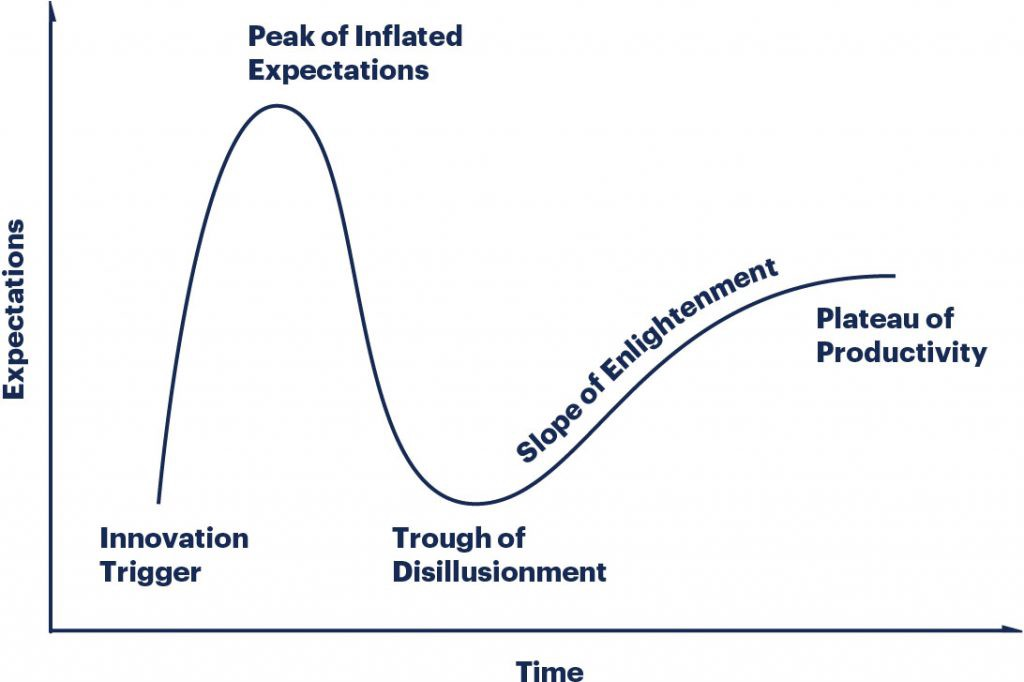

These recent headlines illustrate a sustaining trend when it comes to auto — the correction is here. Indeed, if we look at the Gartner hype cycle, after years of excitement it is safe to say we are well on our way to the Trough of Disillusionment.

Let’s analyze the three main factors, namely investments, acquisitions, and China, in more depth.

1) Less Investments — Auto investments exploded in the last 4 years hugely because of the excitement around autonomous vehicles (AVs). The promise remains but the results are elusive, especially achieving L4 ie that the car can drive without a human. Cruise probably exemplifies this challenge better than any other company, having announced just last month it was delaying its robotaxi service, without giving further details. Cruise was acquired by GM in Mar 2016 for reportedly a billion dollars before having a product fully in the market. Indeed, notwithstanding the incredible talent in the company L4 is just a very very hard problem. VCs have likewise slowed down in their investments on AVs, focusing instead on the next layer of the stack such as V2V and telematics.

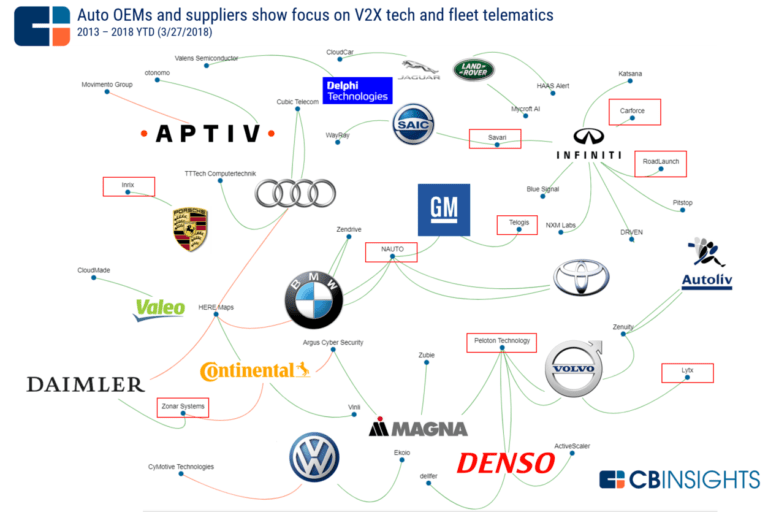

2) More Acquisitions — With less follow-on money available and business models that are not fully working yet, many startups are going to fail. These then become prime targets for consolidation by both Big Tech and increasingly Big Auto which is waking up to software acquisitions. The diagram below shows such acquisitions with orange lines. For completeness, green represents investments and red boxes indicate startups developing V2X and telematics ie the next layer of the stack.

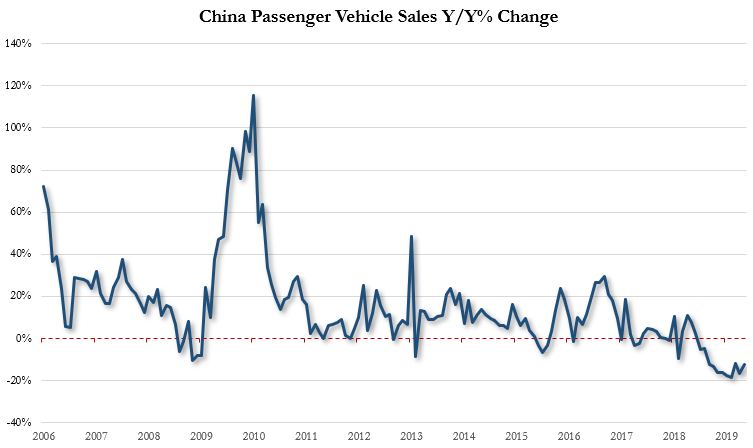

3) China — Their car sales have not just slowed down but actually declined, which is a result of many factors arguably beyond the ongoing trade war with the US. Case in point, their June decline was the 12th in a row and the market is indeed suffering protracted slowdown after decades of growth.

China is the biggest player in auto by several metrics, including electric batteries and VC investments, so the slowdown naturally affects Big Tech, Big Auto and startups globally. What this means for entrepreneurs — don’t count on VC money to be as plentiful or corporates to be as eager to partner as before.

This post is inspired by a conversation with Brent West. These are purposely short articles focused on practical insights (I call it gl;dr — good length; did read); many of my writings can be found here. I would be stoked if they get people interested enough in a topic to explore in further depth. All opinions expressed here are my own. If this article had useful insights for you do give a share, any thoughts comment away.