Carbon Taxes Go Global: How the EU's Climate Tariffs Are Sparking an Economic Revolution

Swagoto Chatterjee·6 min

Even as the U.S. stock market has fallen as a result of the escalation in the U.S. – China trade war, the economy is forecast to grow above trend at 2.1% and 2.0% in 2019 and 2020. Meanwhile, unemployment will remain low, despite rising gradually throughout the forecast period. Inflation is, however, poised to fall to 1.5% while the core measure, which excludes volatile food and energy components will remain close to the Federal Reserve's 2.0% target. It is surprising that the economy is forecast to perform favorably while the stock market woes persist. As such, the Fed’s dovish tilt is explained by the latter even as macroeconomic outcomes appear robust.

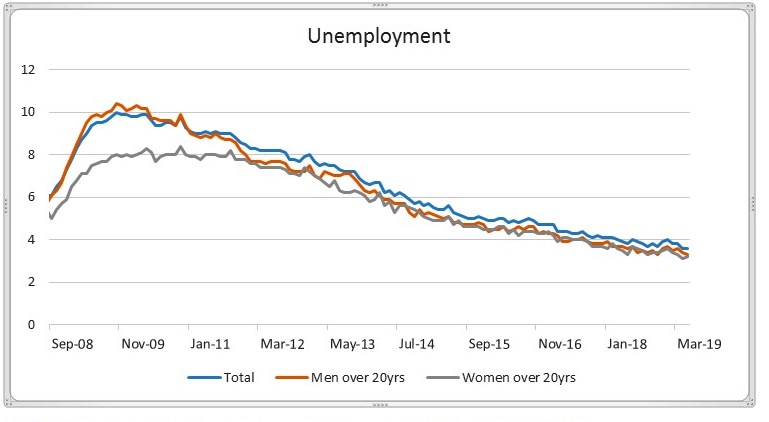

Despite some reservation, for what is originally termed an insurance cut, the stock market as a leading indicator provides sound justification for an upcoming cut. This justification isn’t unassailable. Following the 2018 pro-cyclical fiscal stimulus, the value of U.S. asset prices grew at a much faster pace than wages; this explains why the correction in asset prices has not seen a resounding correction in the real economy. As illustrated in the chart below, unemployment has maintained a steady downtrend and only increased marginally in January.

Even as the U.S. stock market has fallen as a result of the escalation in the U.S. – China trade war, the economy is forecast to grow above trend at 2.1% and 2.0% in 2019 and 2020. Meanwhile, unemployment will remain low, despite rising gradually throughout the forecast period. Inflation is, however, poised to fall to 1.5% while the core measure, which excludes volatile food and energy components will remain close to the Federal Reserve's 2.0% target. It is surprising that the economy is forecast to perform favorably while the stock market woes persist. As such, the Fed’s dovish tilt is explained by the latter even as macroeconomic outcomes appear robust.

Despite some reservation, for what is originally termed an insurance cut, the stock market as a leading indicator provides sound justification for an upcoming cut. This justification isn’t unassailable. Following the 2018 pro-cyclical fiscal stimulus, the value of U.S. asset prices grew at a much faster pace than wages; this explains why the correction in asset prices has not seen a resounding correction in the real economy. As illustrated in the chart below, unemployment has maintained a steady downtrend and only increased marginally in January.

Yield curve overemphasizes structural divergence …Fed cut could signal

Meanwhile, the yield curve inversions overemphasized the structural divergence between the real economy (labor market) and asset prices. As such, the low noise to signal ratio saw the 10yr-2yr and 10yr-3-month treasury curve sends falls recessionary signals. For the latter to predict a recession, a 15bps spread well above 10 days should be a precursor to a 20% correction in financial markets. Nevertheless, a rate cut is all but unjustified even as the Fed might struggle to balance a rate cut unless it lowers the U.S economy’s growth outlook as the impact of the trade war begins to bite, however slowly. Furthermore, if underlying inflationary persist, some might question the legitimacy of rate cuts. But an uncertain outlook appears to be a viable rebuttal.

Meanwhile, the originally termed insurance cut will likely extend the current bull run, incentivize capital flows into riskier assets and support the labor market. Hence the divergence between the real economy and financial markets will likely persist through 2021. By no means, I’m I forecasting a never-ending bull run, but the current financial cycle will likely be extended further.

Is a 2021 recession likely?

The U.S economy has seen its longest bull run on record, with strong economic activity, falling unemployment, rising wage, and asset prices. Nevertheless, the distributional effects of tax cut between asset prices and the real economy were uneven, which explains the lagged response of the U.S labor market to falling asset prices. As such, a rate cut will likely extend the current bull run with unemployment rising only marginally in the coming months. This divergence in accrued benefits in the asset market and lagged labor market response to the impact of the trade war suggest it will be difficult to predict a bull run past 2021- as the conditions will be ripe for a recession.

Yield curve overemphasizes structural divergence …Fed cut could signal

Meanwhile, the yield curve inversions overemphasized the structural divergence between the real economy (labor market) and asset prices. As such, the low noise to signal ratio saw the 10yr-2yr and 10yr-3-month treasury curve sends falls recessionary signals. For the latter to predict a recession, a 15bps spread well above 10 days should be a precursor to a 20% correction in financial markets. Nevertheless, a rate cut is all but unjustified even as the Fed might struggle to balance a rate cut unless it lowers the U.S economy’s growth outlook as the impact of the trade war begins to bite, however slowly. Furthermore, if underlying inflationary persist, some might question the legitimacy of rate cuts. But an uncertain outlook appears to be a viable rebuttal.

Meanwhile, the originally termed insurance cut will likely extend the current bull run, incentivize capital flows into riskier assets and support the labor market. Hence the divergence between the real economy and financial markets will likely persist through 2021. By no means, I’m I forecasting a never-ending bull run, but the current financial cycle will likely be extended further.

Is a 2021 recession likely?

The U.S economy has seen its longest bull run on record, with strong economic activity, falling unemployment, rising wage, and asset prices. Nevertheless, the distributional effects of tax cut between asset prices and the real economy were uneven, which explains the lagged response of the U.S labor market to falling asset prices. As such, a rate cut will likely extend the current bull run with unemployment rising only marginally in the coming months. This divergence in accrued benefits in the asset market and lagged labor market response to the impact of the trade war suggest it will be difficult to predict a bull run past 2021- as the conditions will be ripe for a recession.Henri Kouam Tamto is a macroeconomist focusing on Oil, FX and Credit markets in Advanced and emerging market economies. Working both independently and as part of a team, Henri forecasts and writes both thematic as well as research notes on economic data releases, Central bank policy, and global commodity prices. He also has a strong interest in trade policy and the implications of globalization for countries and asset classes.